A financial revolution is underway, led by fintech. Traditional banking is being challenged, financial services are just a click away, and digital currencies are reshaping money. This dynamic shift is redefining how we manage finances.

However, fintech’s success hinges on navigating regulatory compliance—a complex framework that can either drive innovation or limit potential. The way these regulations are managed will influence consumers, businesses, and economies globally. In this evolving landscape, compliance and risk management are crucial to building trust, security, and stability. Fintech companies must excel in these areas to thrive.

Join us as we explore the strategies behind fintech’s growth, uncovering how innovation and compliance come together to shape the future of finance.

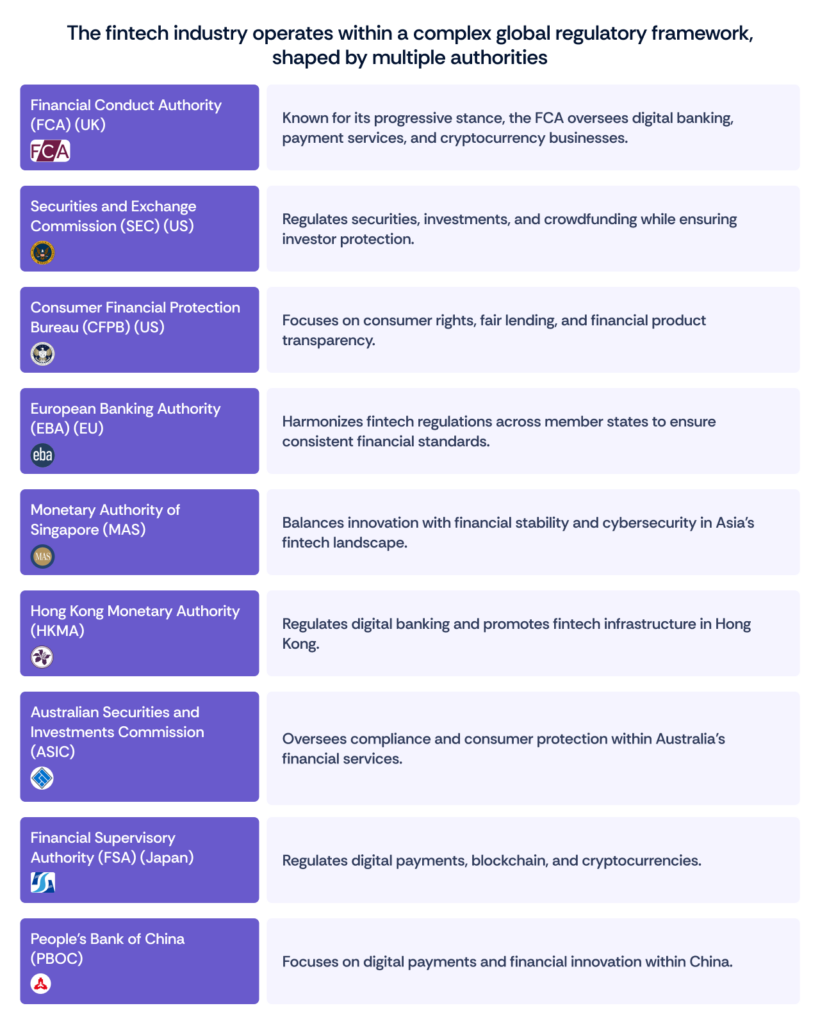

What are the current fintech regulations and standards?

These regulatory bodies are responsible for developing and enforcing regulations that govern fintech operations, ensuring compliance with financial laws, protecting consumers, and maintaining the stability of the financial system. Staying informed about the regulations set forth by these authorities is essential for Fintech companies to operate legally and responsibly in the global financial ecosystem.

Read also: Role of information security in the changing Indian fintech landscape

What is fintech compliance?

Fintech compliance refers to the set of rules, regulations, and standards that fintech companies must adhere to in order to operate legally and responsibly within the financial industry. It encompasses the processes and measures fintech firms put in place to ensure that their operations, products, and services comply with relevant laws and regulations.

Fintech compliance is essential for maintaining the integrity of financial markets, protecting consumers, and preventing financial crimes such as money laundering and fraud.

What are fintech compliance regulations?

Compliance in the fintech industry is multifaceted, encompassing various regulatory requirements and expectations that fintech companies must meet to operate legally and responsibly.

Here are some of the key compliance requirements and expectations:

A. Anti-money laundering (AML) and KYC compliance

Fintech firms are required to establish and maintain robust AML and KYC procedures. This involves verifying the identities of customers, conducting due diligence to detect and prevent money laundering, and reporting suspicious activities to relevant authorities. The depth and stringency of AML and KYC procedures may vary depending on the jurisdiction and the nature of the fintech services offered.

B. Data protection and privacy

With the handling of sensitive customer data, compliance with data protection and privacy regulations is paramount. In the European Union, the General Data Protection Regulation (GDPR) sets strict standards for data privacy and requires fintech companies to obtain explicit consent for data processing, provide data access to customers, and implement data breach notification protocols. Similar regulations exist in various countries and regions.

C. Payment services regulations

Fintech companies that offer payment processing services must adhere to specific payment services regulations. For instance, the revised Payment Services Directive (PSD2) in the European Union regulates payment service providers, mandates strong customer authentication, and promotes open banking practices.

D. Cybersecurity and data security

Given the digital nature of fintech, cybersecurity is of utmost importance. Compliance expectations include implementing robust cybersecurity measures to protect customer information, financial data, and systems from cyber threats and data breaches. Fintech companies may need to undergo security audits and penetration testing to ensure the security of their platforms.

E. Consumer protection

Fintech firms are expected to provide transparent, fair, and accessible financial services to consumers. This includes clear disclosure of terms and fees, addressing customer complaints promptly, and ensuring financial inclusion by serving underserved populations. Regulatory authorities often scrutinize advertising practices and the presentation of financial products to prevent misleading marketing.

F. Regulatory reporting

Fintech compliance may involve regular reporting to regulatory authorities, including financial statements, operational data, and other relevant information. These reports help regulators monitor the activities of Fintech firms and ensure adherence to regulations.

G. Cross-border compliance

If a fintech company operates internationally, it must navigate the complexities of complying with different regulatory regimes across borders. Harmonization efforts and international cooperation are emerging trends to address this challenge.

H. Innovation testing and regulatory sandboxes

Some jurisdictions offer regulatory sandboxes or innovation testing frameworks that allow fintech startups to test their innovative products and services in a controlled environment, facilitating compliance testing before full-scale market entry.

Compliance in fintech is not only a legal obligation but also essential for building trust among customers and investors. Fintech companies must stay vigilant, adapt to evolving regulations, and invest in compliance programs to thrive in a rapidly changing industry while ensuring the safety and security of financial services for all stakeholders.

Read also: Revolutionizing the Fintech compliance game with Regusense: A Unified Control Framework

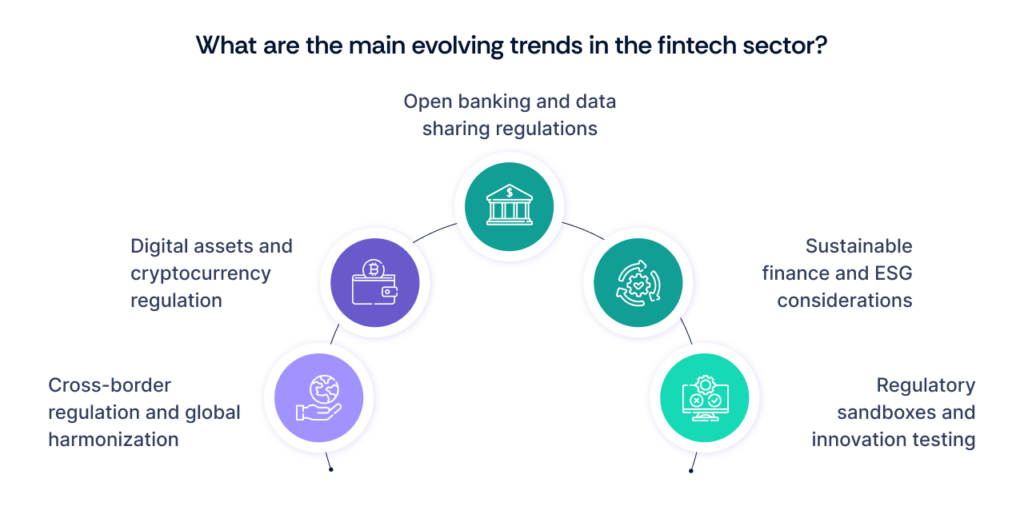

What are the evolving regulatory trends and their impact on fintech?

The fintech industry operates in a dynamic regulatory landscape where evolving trends have a profound impact on how fintech companies operate, innovate, and compete. Understanding these trends is essential for fintech firms to adapt and thrive.

Here are some of the key evolving regulatory trends and their impact on the fintech sector:

A. Cross-border regulation and global harmonization

Trend: Fintech companies often operate across borders, making compliance with different regulatory regimes complex and challenging. To address this, there is a growing trend toward cross-border regulatory cooperation and harmonization efforts. Regulatory authorities in different countries are working together to create consistent standards and streamline compliance for fintech firms with a global presence.

Impact: This trend reduces compliance burdens for fintech companies operating internationally, fosters innovation and facilitates expansion into new markets. It also enhances regulatory clarity and reduces uncertainty.

B. Digital assets and cryptocurrency regulation

Trend: The rise of cryptocurrencies, digital assets, and blockchain technology has led to increased regulatory scrutiny. Governments and regulatory bodies are developing frameworks to regulate these digital assets, balancing innovation with investor protection and financial stability.

Impact: Fintech companies involved in cryptocurrency trading, blockchain-based services, and digital wallet offerings must navigate evolving regulations. Clear regulatory frameworks can provide legitimacy to the cryptocurrency industry while addressing concerns about fraud, money laundering, and market manipulation.

C. Open banking and data sharing regulations

Trend: Open banking regulations, such as PSD2 in the European Union, mandate that banks provide access to customer data to third-party fintech providers through Application Programming Interfaces (APIs). Similar initiatives are emerging worldwide, allowing customers to share their financial data securely with fintech firms.

Impact: Open banking regulations promote competition, innovation, and the development of new financial services. Fintech firms can leverage customer data to create personalized and efficient solutions. Fintech compliance involves meeting security and data protection standards while ensuring customer consent and data portability.

D. Sustainable finance and ESG considerations

Trend: Environmental, social, and governance (ESG) considerations are becoming increasingly important in the financial industry. Regulatory bodies are developing frameworks and disclosure requirements to promote sustainable finance and ESG-focused investments.

Impact: Fintech companies are expected to align their services with ESG principles and disclosure requirements. This trend opens opportunities for fintech firms to create sustainable investment products and environmentally friendly financial solutions.

E. Regulatory sandboxes and innovation testing

Trend: Many regulatory authorities are establishing regulatory sandboxes or innovation testing frameworks. These programs allow fintech startups to test innovative products and services in a controlled environment while working closely with regulators to ensure compliance.

Impact: Regulatory sandboxes foster innovation by providing a safe space for experimentation. Fintech startups can refine their products and services, gain regulatory feedback, and ensure fintech compliance before launching in the broader market.

Staying informed about these evolving regulatory trends is crucial for fintech companies to proactively adapt their strategies, fintech compliance programs, and business models. Adherence to emerging fintech regulatory standards not only ensures legal compliance but also enhances trust among customers and partners, facilitating growth and sustainability in the fintech industry.

Read also: Why is compliance more than just a tick box for Indian Fintech companies?

What are the strategies for fintech regulatory compliance and risk mitigation?

Ensuring regulatory compliance and mitigating risks are critical for Fintech companies to operate successfully.

Here are strategies that combine both regulatory compliance and risk mitigation efforts:

A. Develop a compliance framework

- Culture of compliance: Foster a corporate culture that places a high value on regulatory compliance. Ensure all employees understand their role in upholding compliance standards.

- Compliance officers and teams: Appoint dedicated compliance officers and teams responsible for overseeing compliance efforts. They should have the expertise to navigate regulatory requirements effectively.Often, these teams work alongside a FinTech software development company to ensure that compliance protocols are technically integrated into the product architecture.

- Comprehensive policies and procedures: Develop and maintain comprehensive compliance policies and procedures that align with specific regulatory mandates. These documents should provide clear guidance on handling compliance-related matters.

B. Risk assessment and management

- Identify and assess risks: Conduct thorough risk assessments to identify potential compliance risks and operational vulnerabilities. Evaluate the impact of non-compliance on the business.

- Risk mitigation strategies: Develop tailored risk mitigation strategies based on identified risks. These may involve enhancing cybersecurity measures, improving AML and KYC procedures, and creating contingency plans.

C. Compliance monitoring and reporting

- Regular audits and assessments: Establish a process for conducting regular internal audits and assessments to ensure ongoing compliance. Cover all aspects of regulatory compliance and risk management.

- Prompt reporting: Implement mechanisms to report compliance-related information to regulatory authorities as required. Timely reporting of incidents such as suspicious activities, data breaches, or fraud is crucial.

D. Regulatory technology (RegTech) solutions

Leverage RegTech solutions to automate compliance tasks and enhance risk management. RegTech tools can streamline AML and KYC processes, facilitate reporting, and improve monitoring capabilities.

E. Collaboration with regulators and industry peers

Engage in open dialogue with regulatory authorities to stay informed about compliance expectations and regulatory changes. Collaborate with industry peers to share best practices and address common compliance and risk challenges.

F. Stay informed and adapt

Continuously monitor regulatory changes and updates relevant to your fintech operations. Adapt your compliance and risk mitigation strategies accordingly to remain aligned with evolving requirements.

G. Education and training

Provide ongoing education and training to employees on compliance and risk management. Equip them with the knowledge and skills needed to recognize and address compliance-related issues effectively.

H. Third-party due diligence

If your fintech company relies on third-party vendors or partners, conduct due diligence to ensure they also adhere to relevant compliance standards. Verify that their practices align with your own compliance requirements.

I. Document and maintain records

Keep detailed records of compliance-related activities, audits, assessments, and reports. Proper documentation is essential for demonstrating compliance to the regulators and stakeholders.

J. Customer communication

Maintain transparent communication with customers regarding data collection, usage, and protection. Address their privacy concerns and ensure compliance with data protection regulations.

K. Market and operational risk mitigation

Implement strategies to mitigate market and operational risks, such as system failures, scalability challenges, and regulatory changes. Diversify product offerings and maintain contingency plans.

By combining these strategies, Fintech companies can effectively manage regulatory compliance and mitigate risks in an ever-evolving and dynamic industry landscape. This proactive approach not only helps in legal adherence but also enhances trust among customers and partners, supporting long-term growth and sustainability.

Read also: How can Fintech Startups Create an Enterprise-Friendly InfoSec Posture

What are the anticipated fintech regulatory changes?

As the Fintech industry continues to evolve, regulatory changes are expected to play a significant role in shaping its future. Anticipated regulatory changes include:

- Enhanced data privacy regulations: Anticipate stricter data privacy regulations to protect consumer data. Fintech companies will need to invest in robust data protection measures and compliance with emerging privacy standards.

- Digital asset and cryptocurrency regulations: Expect continued efforts by regulators to establish clearer frameworks for the use of digital assets, cryptocurrencies, and blockchain technology. These regulations aim to strike a balance between innovation and investor protection.

- Cross-border regulatory cooperation: Regulatory authorities worldwide may increasingly collaborate to harmonize regulations for fintech firms operating across borders, reducing compliance complexities for international expansion.

- Sustainable finance requirements: As ESG considerations gain prominence, anticipate regulations promoting sustainable finance and green investments. Fintech companies will need to align their services with these principles.

Read also: Navigating PCI DSS compliance: A comprehensive checklist

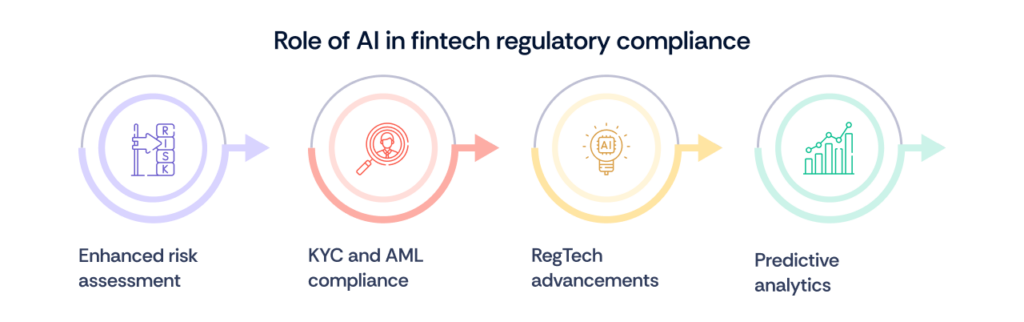

What is the role of artificial intelligence (AI) and automation in fintech regulatory compliance?

The integration of AI and automation technologies is poised to revolutionize fintech compliance. AI-driven solutions will not only enhance risk assessment and fraud detection but also streamline regulatory processes.

- Enhanced risk assessment: AI and automation will play a more significant role in risk assessment, enabling Fintech companies to identify and mitigate compliance risks more efficiently.

- KYC and AML compliance: AI-driven KYC and AML solutions will become more sophisticated, improving customer onboarding processes and enhancing fraud detection.

- RegTech advancements: The adoption of RegTech will increase streamlining compliance processes, automating reporting, and reducing compliance-related costs.

- Predictive analytics: AI will be used for predictive analytics to anticipate regulatory changes and their potential impact, allowing fintech firms to proactively adjust their compliance strategies.

Read also: Navigate the AI Compliance Landscape Confidently

How to prepare your organization for a dynamic regulatory landscape?

To thrive in the ever-evolving world of fintech compliance, companies must be prepared for a regulatory landscape that is continuously shifting. This involves cultivating adaptability, embracing technology, and fostering a deep understanding of both local and global compliance requirements.

- Continuous monitoring: Use regulatory intelligence tools to stay updated and adapt swiftly to changes.

- Agility and flexibility: Build compliance frameworks that can quickly adjust to evolving regulations.

- Regulatory sandboxes: Test new products under regulatory supervision before full-scale launch.

- Cross-functional collaboration: Align compliance, legal, and tech teams for a comprehensive approach.

- Global regulatory expertise: Invest in local regulatory knowledge when expanding internationally.

- Ethical considerations: Ensure compliance aligns with corporate values and social responsibilities.

Navigating fintech compliance requires a proactive approach, combining technology, regulatory intelligence, and agility. Fintechs that prioritize compliance and embrace innovation will be best positioned to thrive in this evolving landscape.

Listen to:

AI With a Pinch of Responsibility

Final words

In the fast-evolving world of fintech, regulatory compliance and risk management are essential for trust and stability. As fintech reshapes finance, understanding regulations is critical. Key areas include anti-money laundering, data protection, payment services, and cybersecurity—safeguarding both consumers and financial integrity.

To succeed, fintechs must foster a compliance culture, conduct risk assessments, and use RegTech solutions. Collaboration with regulators and industry peers is also crucial. AI and automation are transforming compliance, enhancing fraud detection and risk management.

Adapting to trends like enhanced data privacy, digital asset regulations, open banking, and sustainability is vital. Fintech’s success lies in balancing innovation with compliance to build trust and thrive in this dynamic landscape.

Stay Ahead of Fintech Regulations with Scrut

Navigate the complexities of fintech compliance with ease. Scrut’s all-in-one platform empowers you to manage regulatory requirements, mitigate risks, and stay agile in an ever-evolving landscape. Ensure trust, security, and success—partner with Scrut today and future-proof your fintech operations!

Fintech regulatory compliance refers to the set of rules, regulations, and standards that fintech companies must adhere to in order to operate legally and responsibly within the financial industry. It covers various aspects such as anti-money laundering, data protection, cybersecurity, and more.

Fintech compliance is essential for maintaining the integrity of financial markets, protecting consumers, and preventing financial crimes such as money laundering and fraud. It builds trust among customers, investors, and regulators, fostering long-term sustainability in the industry.

AI plays a significant role in enhancing risk assessment, automating compliance processes, and improving fraud detection. It enables fintech companies to navigate compliance requirements more efficiently and proactively.

Best practices include conducting regular risk assessments, developing tailored risk mitigation strategies, implementing compliance monitoring and reporting mechanisms, and embracing AI-driven solutions for risk management.

Fintech companies can stay agile by maintaining flexible compliance frameworks, continuously reviewing and updating policies, and participating in regulatory sandboxes when available. Regular engagement with regulatory authorities helps anticipate and adapt to changes effectively.

.png)